Article

How to Read a Condo Financial Statement

Understanding a condo financial statement is crucial for condo owners, board members, investors, and property managers. It provides a snapshot of the condominium association’s financial health, detailing revenue, expenses, assets, liabilities, and reserves. Whether you're evaluating your monthly dues, potential special assessments, or overall financial sustainability, knowing how to interpret this document ensures informed decision-making.

1. What Is a Condo Financial Statement?

A condo financial statement is a formal report prepared by the condo association or its management company, typically monthly, quarterly, or annually. It provides insight into:

Income sources – Condo fees, special assessments, and other revenue streams.

Expenses – Maintenance, utilities, management fees, insurance, and capital improvements.

Assets and Liabilities – Cash, outstanding debts, and fund balances.

Reserve Fund – Savings for major repairs and replacements.

A condo board relies on this financial statement to assess financial stability, plan budgets, and ensure long-term property maintenance.

2. Key Components of a Condo Financial Statement

A standard condo financial statement consists of four primary sections:

A. Balance Sheet (Statement of Financial Position)

The balance sheet presents the condo association’s financial health at a specific point in time. It’s divided into three main categories:

1. Assets (What the Condo Owns)

Cash and Cash Equivalents: Funds in the operating and reserve accounts.

Accounts Receivable: Unpaid condo fees from owners.

Fixed Assets: Property owned by the association (e.g., office equipment, maintenance tools).

2. Liabilities (What the Condo Owes)

Accounts Payable: Bills owed (contractor payments, utilities, legal fees).

Long-Term Debt: Outstanding loans or mortgages.

Prepaid Assessments: Condo fees paid in advance by owners.

3. Fund Balances (Equity of the Association)

Operating Fund Balance: Funds for day-to-day expenses.

Reserve Fund Balance: Money saved for major repairs.

Accumulated Surplus or Deficit: Net funds after expenses.

What to Watch For:

✅ Positive fund balance indicates financial health.

❌ Negative fund balance suggests financial instability.

B. Income Statement (Profit and Loss Statement)

The income statement details financial activity over a specific period (monthly, quarterly, or yearly). It is divided into:

1. Revenue (Income Sources)

Maintenance Fees / Condo Assessments: Regular fees collected from owners.

Special Assessments: One-time fees for major projects.

Other Income: Rental income, parking fees, fines, investment earnings.

2. Expenses (Operating Costs)

Utilities (Electricity, Water, Gas)

Repairs and Maintenance (Landscaping, Elevators, Plumbing, HVAC)

Insurance (Property, Liability)

Management Fees (Property Management Company)

Legal and Professional Fees (Audits, Legal Disputes)

3. Net Income or Deficit

If revenues exceed expenses → SURPLUS (good financial health).

If expenses exceed revenues → DEFICIT (possible financial issues).

Red Flags:

❌ Recurring deficits may indicate mismanagement.

❌ Frequent special assessments suggest inadequate budgeting.

C. Statement of Cash Flows

This report tracks cash movements and is divided into:

Operating Activities: Condo fees collected and daily expenses paid.

Investing Activities: Large-scale renovations, equipment purchases.

Financing Activities: Loans, special assessments, reserve fund contributions.

✅ Positive cash flow means the association is collecting enough revenue.

❌ Negative cash flow suggests financial problems.

D. Reserve Fund Report

The reserve fund is a long-term savings account for major repairs (e.g., roof replacement, elevator upgrades, repaving).

A healthy reserve fund ensures financial stability and avoids unexpected assessments on condo owners.

Key Aspects:

Current Reserve Balance – How much is in reserves.

Annual Contributions – How much is being saved each year.

Planned Future Expenditures – Projected costs for major repairs.

✅ A well-funded reserve ensures smooth operations.

❌ An underfunded reserve means potential financial stress for owners.

3. Warning Signs of Financial Trouble

High delinquency rates (unpaid condo fees).

Frequent special assessments.

Low reserve fund balances.

Negative cash flow.

A condo financial statement is an essential tool for evaluating financial stability, planning for major repairs, and ensuring the association is well-managed. Reviewing these documents regularly helps condo owners avoid financial surprises and ensures long-term property value.

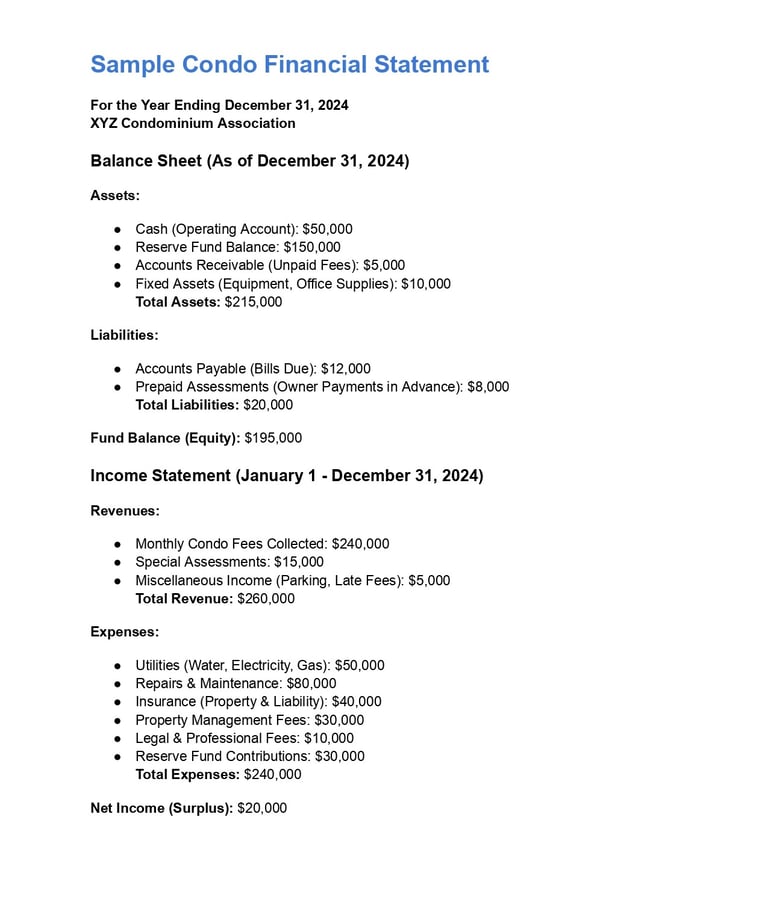

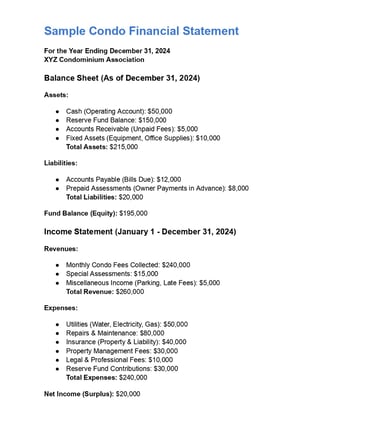

Sample Condo Financial Statement

Disclaimer: This is a sample financial statement for informational purposes only. Actual financial statements may vary based on specific association policies, accounting methods, and financial conditions. Consult a certified accountant or property management professional for accurate financial reporting.